Mortgage Rates in Canada

How Are They Determined?

Mortgage rates in Canada have increased dramatically since February 2022. We became accustomed to a low-rate environment, encouraged by the Bank of Canada’s assurances that interest rates would stay low for a long time, and this sudden change has caught many by surprise.

Why Are Mortgage Rates Increasing in Canada?

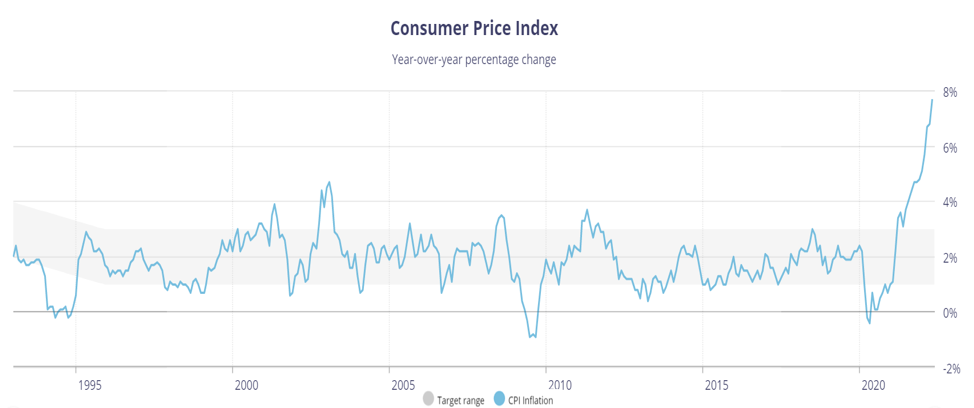

The simple answer is inflation (measured using the Consumer Price Index). This time last year there were signals that inflation was coming but the central banks told us not to worry about it. They said it would be transitory. How were the supposed economic experts so wrong?

Source: The Bank of Canada

The Bank of Canada manages the supply of money circulating in the economy. It sets interest rates as part of its monetary policy framework to keep inflation low and stable. They set targets for inflation, with recent targets being about 2%. If inflation rises beyond that level a central bank will usually increase interest rates to curb demand in the market, tighten the money supply and bring inflation back to their target.

As we have recently experienced, inflation has not just risen above 2%, it has spiked to 8% in Canada. The Bank of Canada has aggressively increased rates in response to this spike in inflation. This has resulted in an increase in mortgage rates.

How Are Mortgage Rates Set?

There are two main types of mortgage rates – fixed rates and variable rates.

Fixed Rate Mortgages

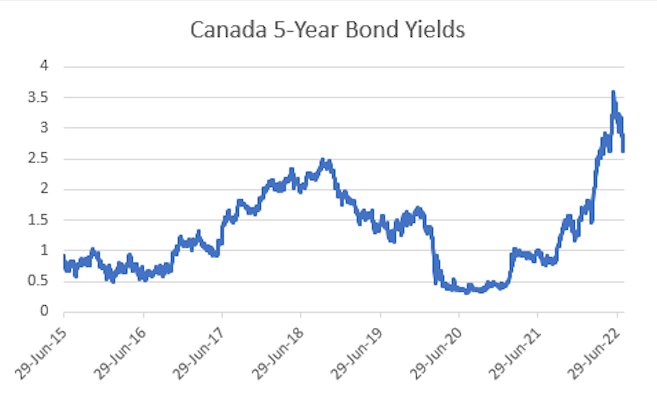

Fixed rate mortgages are primarily priced off the bond market. Much of the funding for fixed rate mortgages is raised in the bond market (plus the deposit market for banks). The rate on a fixed-rate mortgage is determined by a mortgage lender by adding their costs plus their desired profit margin to their cost of funding in the bond market. In other words, they take the interest rate on the bond and add their required margin to cover expenses and earn income.

As bond rates change, fixed mortgage rates change. Through the spring and early summer, yields on bonds have increased in response to inflation concerns and this has pushed up the rates on fixed rate mortgages.

Source: The Bank of Canada

Variable Rate Mortgages

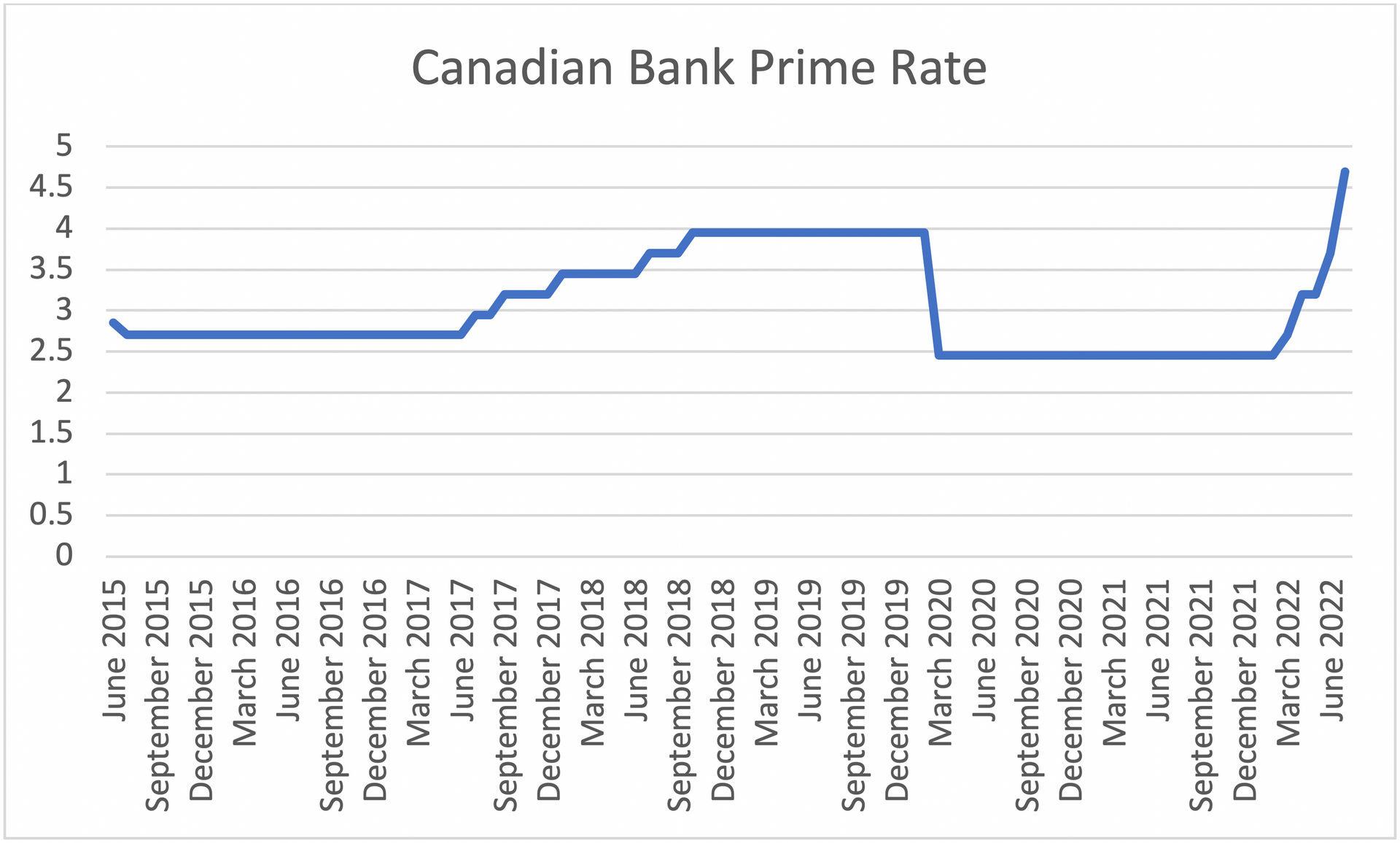

Variable-rate mortgages are priced relative to the Prime rate. This is the annual rate of interest that our major banks use to set the rates on their variable rate lending products, like mortgages and lines of credit. The Bank of Canada has its own target interest rate, known as the overnight rate. This is the base rate at which banks can borrow and they base their Prime rate off this rate. When the Bank of Canada changes the overnight rate, banks usually change their Prime rates by an equivalent amount in response.

Source: Bank of Canada

The rate on a variable-rate mortgage is determined by a mortgage lender using Prime as the benchmark. The lender determines the variable rate that provides them their required margin over their short-term funding costs and references it to the Prime rate. In most cases, the variable mortgage rate will be Prime minus a spread.

Variable rates are usually lower than fixed rates. This can present advantages, both in terms of lower mortgage payments at the time of taking out the mortgage as well as being able to qualify with a lower rate. However, there are risks with variable rate mortgages that should not be ignored:

1. Your monthly payment can increase if rates increase,

2. Even if you have a static payment, it may increase if your mortgage rate reaches the trigger rate,

3. You may also be required to make lump sum payments to bring the mortgage amortization back in line if you have a static payment and rates increase.

Fixed rate mortgages may have higher rates, but that higher rate is essentially the cost of insurance against the negative consequences should interest rates increase.

Will Mortgage Rates Change in the Future?

Mortgage rates will change over time. They could go down if bond market interest rates decline or if the Prime rate declines. Likewise, they could go up. Unfortunately, no one has a crystal ball that can tell them exactly where rates are going. There are many so-called experts out there making predictions, but most of them completely missed this recent significant increase in rates. This shows how hard it is to predict the future direction of interest rates. We can make predictions, but we will usually find that we are wrong.

As a mortgage borrower it is more important to understand what a change in mortgage rates, in either direction, can mean to you. Will it impact your current mortgage payments? Will it impact your financial situation if you have to renew your current mortgage?

Another key consideration is your tolerance for risk. Most prudent corporations hedge their interest rate risk so they don’t suffer negative consequences if rates increase. This may mean missing out on the benefit of a decline in rates, but it is considered prudent financial management. We think most individuals should consider this as well. Maybe there is a good reason to take interest rate risk and you understand and can afford the downside. But if this is not the case, remember we are talking about financing your home. Fixed rate mortgages have historically been the most popular choice for borrowers in Canada who prefer being safe and prudent. The peace of mind from a fixed rate mortgage has value and keeps you from having to always worry about changing interest rates. They will change and it is on all of us to prepare ourselves for that to happen.

Who Offers the Best Mortgage Rates in Canada?

There are three main types of mortgage lenders in Canada:

1. Banks

2. Credit Unions

3. Mortgage Companies (often called monoline lenders).

All lenders compete for your business. No one lender, nor category of lenders, consistently has the best rates. There are more than thirty lenders to choose from and it pays to shop around.

You will often find that mortgage brokers can offer mortgage rates that are better than the rates you can find at your bank. If you walk into a bank branch you will get an offer for a mortgage at a certain rate. It will rarely ever be the lowest rate in the market. That same bank may even offer rates through brokers that are lower than the rate they showed you! It does pay to shop around.

There are often times in the market when one lender or another has special offers available. They do not last forever, and you won’t find out about them if you don’t shop around. Often, new borrowers will review several websites looking for the best rates, but this can be tedious and time consuming.

You should also note that insured mortgage rates are usually lower than uninsured mortgage rates. This may seem odd since insured mortgages usually have loan-to-value (LTV) ratios between 80% and 95%, while uninsured mortgages have LTV ratios below 80%. The lower LTV ratio indicates lower risk, but credit risk is not the only pricing determinant. The insured mortgages have a high degree of liquidity, which means they can be funded cheaply in the capital markets via a variety of sources. Uninsured mortgages are not as liquid, and this results in their rates being higher. However, this pricing difference is largely reduced by the mortgage insurance premium you must pay for a lower rate insured mortgage.

What Can I Do to Qualify for the Best Mortgage Rates?

Aside from economic factors like inflation and internal pricing considerations for banks, your own personal situation also affects the mortgage rate you will be offered. The borrowers considered the best, or of the highest credit quality, receive the lowest rates. Borrowers that are considered riskier will be offered higher rates. Some may even be declined for a mortgage.

What are the typical characteristics of the best borrowers? There can be variations between lenders about this, but the best mortgage applications have the following characteristics:

1. High credit scores;

2. Stable employment;

3. Verifiable income;

4. Sufficient down payment;

5. Lower loan-to-value ratios;

6. The purpose of the loan is for a primary residence.

You may still qualify for a mortgage if these features are not all present, but you may not qualify for the lowest mortgage rates.

Where Can I Find the Lowest Mortgage Rates and Make Comparisons?

With fintech companies entering the Canadian mortgage market, access to information is improving for borrowers. The current market, which can sometimes see you get a mortgage, only to find out after closing that there were better deals available that you never saw, is a market that poorly serves its customers. Things will improve. Customers need to embrace this and encourage the work toward an open and transparent model that shows the customer what is possible. This is the mission of Frank Mortgage.

At Frank Mortgage we want to enable financial decision making that is within every individual’s personal control. You can, and should, have more control over your finances. This includes having access to an open marketplace where you can shop for mortgage rates and terms that matter to you. You do not need to search everywhere. At Frank Mortgage, for the first time in Canada, you can now apply once for a mortgage and see what the marketplace of lenders will offer you, all in one place.

Looking for the best mortgage rates in Alberta?

Looking for the best mortgage rates in Ontario?

Looking for the best mortgage rates in New Brunswick?

Looking for the best mortgage rates in British Columbia?

Find us online at www.frankmortgage.com or call us at 1-888-350-1337.

About The Author

Don Scott

Don Scott is the founder of a challenger mortgage brokerage that is focused on improving access to mortgages. We can eliminate traditional biases and market restrictions through the use of technology to deliver a mortgage experience focused on the customer. Frankly, getting a mortgage doesn't have to be stressful.

Related Posts

Learn More

What’s Next?

Join our email community

Sign up with your email address to receive news and updates.

Join Our Email Community

Mortgage Brokerage Licensed in Ontario (#13204), British Columbia, Alberta, Saskatchewan (#514115), Manitoba, Nova Scotia, Newfoundland & Labrador, and New Brunswick (#230015752).

© Frank Mortgage 2025 | All Rights Reserved